It feels like we’ve been holding our breath for years, doesn’t it? Waiting for that magical moment when prices drop, rates plummet, and the "For Sale" signs start looking less like threats and more like invitations. But here we are in May of 2026, and the air hasn’t exactly cleared. If anything, the fog has just shifted shape. You open your news feed and see another headline about mortgage rates climbing back up to 6.30%. You check your grocery bill, then your rent statement, and wonder if buying a home is even a realistic goal anymore or just a fantasy we keep chasing.

The term "sticky inflation" gets thrown around by economists in suits, but for most of us, it just means everything stays expensive for longer than we hoped. It’s not a sudden spike; it’s a slow, grinding pressure that makes every financial decision feel heavy. Especially when it comes to housing. The dream of homeownership isn’t dead, but it has definitely changed clothes. It’s no longer about finding the perfect picket fence house on day one. It’s about strategy, patience, and sometimes, getting a little creative with what you thought was possible.

We’re not going to sugarcoat it. The market is tough. Shelter costs—rent and owners’ equivalent rent—are still the biggest driver of inflation, rising about 3.0% recently. This keeps the Federal Reserve in a tight spot, which keeps borrowing costs high. But knowing why it’s hard doesn’t pay the down payment. What does help is understanding the lay of the land right now, in this specific moment of 2026, and figuring out how to move through it without losing your mind or your savings. Let’s dig into what’s actually happening and how you can make it work.

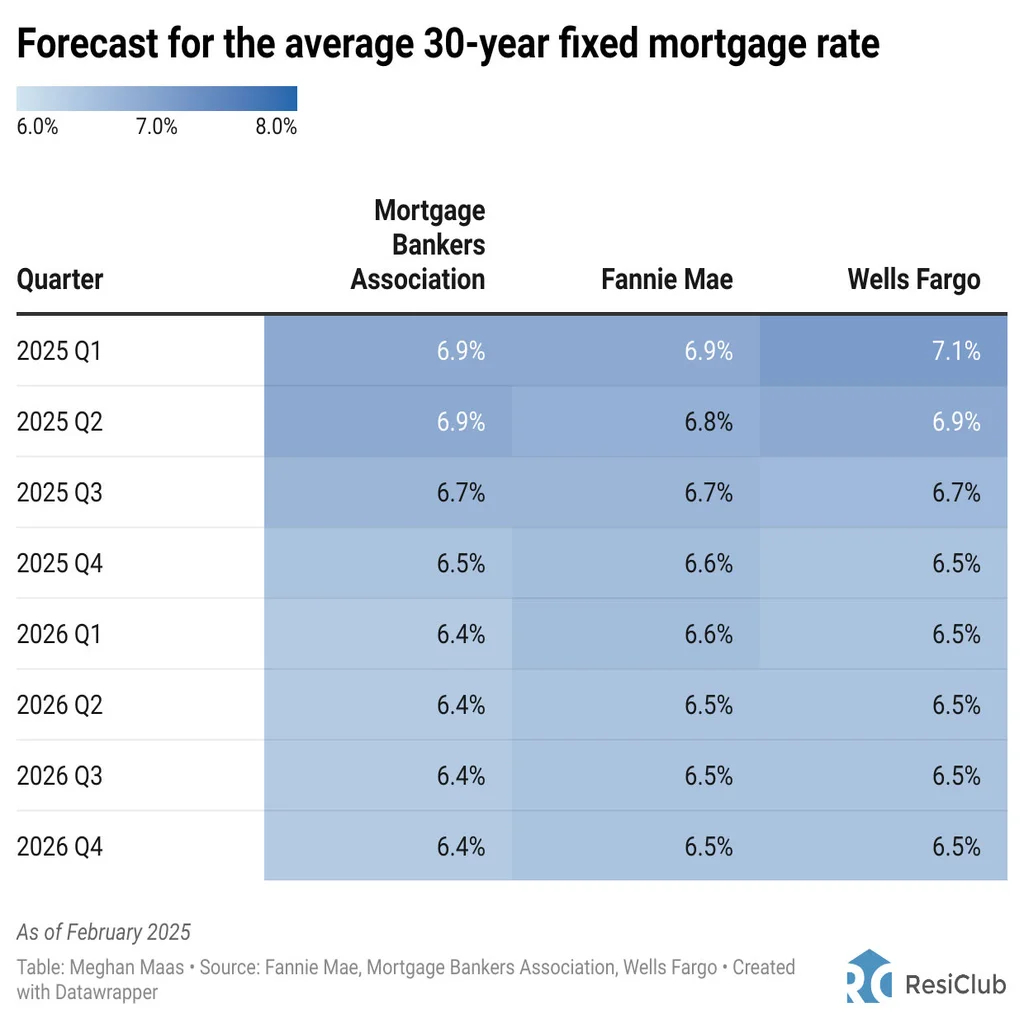

The Rate Reality Check: Why 6% Is the New Normal

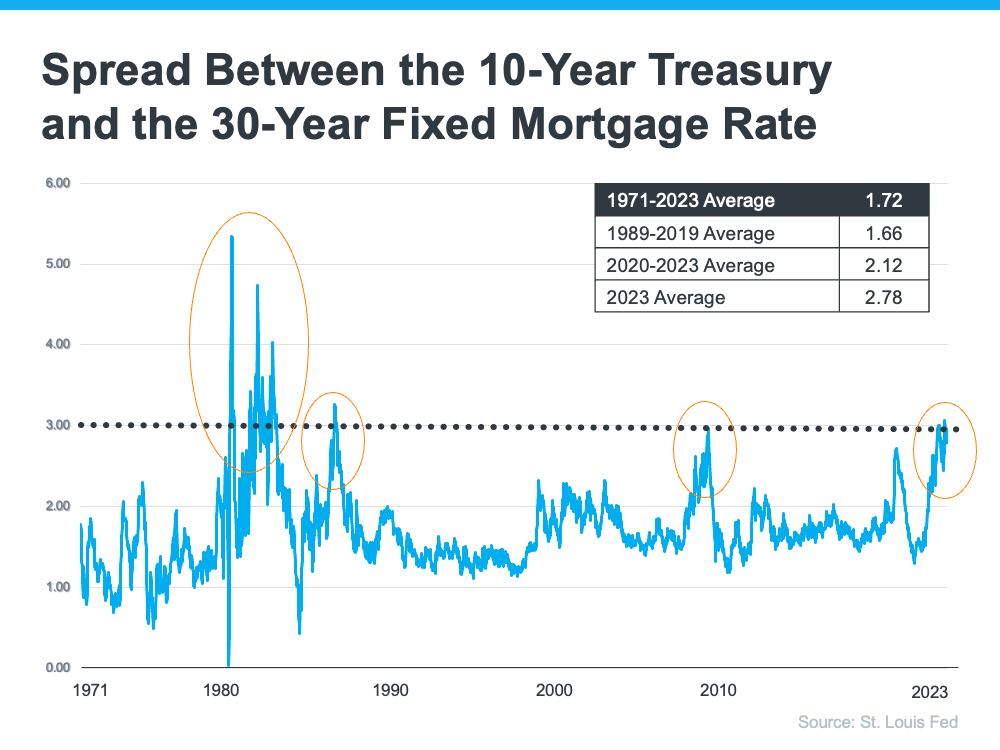

Let’s talk about the elephant in the room: mortgage rates. For a long time, we were obsessed with the idea that rates would drop back to the 3% or 4% range. We waited. And waited. Now, experts are saying that rates will likely stay between 6% and 6.5% for the rest of 2026. That’s a hard pill to swallow. When you look at the numbers, rising Treasury yields and stubborn inflation are the culprits. The Fed wants to cut rates, but they can’t do it aggressively while housing costs keep pushing overall inflation up. It’s a bit of a catch-22.

So, what does this mean for your monthly budget? It means the "lock-in effect" is still very real. People who bought or refinanced at ultra-low rates aren’t moving because they don’t want to trade a 3% rate for a 6.3% one. This limits the supply of existing homes on the market. Fewer homes for sale means prices don’t drop as much as buyers hope, even if demand cools off slightly. You’re competing for a smaller pool of houses, and the financing is more expensive. It’s a double whammy.

But here’s the thing: waiting for rates to crash might cost you more in the long run. If home prices continue to creep up due to low inventory, the slight decrease in your interest rate later might not offset the higher purchase price. Some buyers are starting to realize this. They’re accepting that 6.3% is the current reality. It’s not ideal, but it’s manageable if you adjust other parts of the equation. Stop fixating on the rate alone and start looking at the total monthly cost. Can you live with that number? If yes, then the rate becomes just a detail, not a dealbreaker.

The Shelter Trap: How Housing Costs Keep Prices High

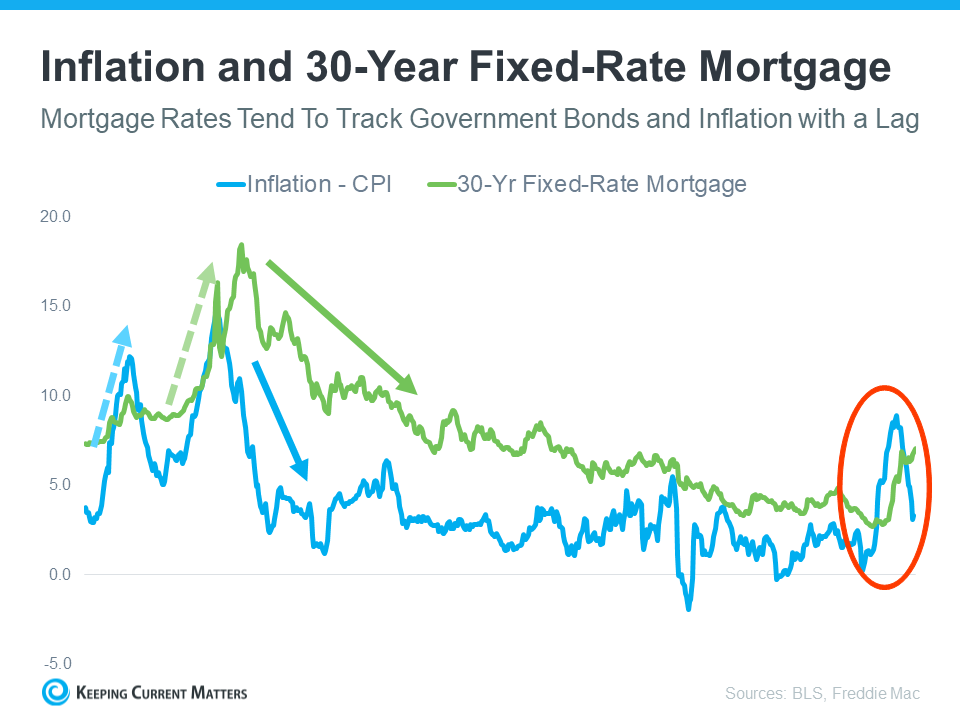

You might have heard that inflation is cooling down in other areas, like used cars or electronics. But housing? That’s a different story. Shelter CPI rose 3.0% in early 2026, making it the single biggest contributor to inflation. This is crucial to understand because it explains why the Fed is hesitant to slash rates. As long as housing costs are rising, overall inflation looks sticky. And as long as inflation looks sticky, mortgage rates stay elevated. It’s a cycle that feels impossible to break from the outside.

This impacts you directly in two ways. First, rents are staying high, which makes saving for a down payment incredibly difficult. If you’re paying a large chunk of your income to a landlord, you have less left over to stash away for your own place. Second, because construction costs (labor, materials, insurance) are also inflated, builders aren’t slashing prices on new homes. They can’t afford to. So, you don’t get the bargain basement deals you might see in other recessions. The floor has moved up.

For low- and moderate-income households, this is particularly brutal. Surveys from places like the Federal Reserve Bank of Cleveland show that service providers are seeing increased stress among families trying to secure stable housing. It’s not just about buying; it’s about basic stability. If you’re in this group, traditional advice like "just save more" doesn’t help when your expenses are rising faster than your wages. You need targeted strategies, like looking into first-time buyer programs that specifically address high-cost areas, or considering co-buying with family members to split the burden.

The Inventory Illusion: Why There Are No Houses to Buy

One of the most frustrating parts of 2026 is looking at Zillow or Redfin and seeing… nothing. Or rather, seeing things that are either way out of your budget or in terrible condition. This isn’t an accident. It’s a structural issue. We have a long-term shortage of housing supply that predates the recent inflation spike. We simply didn’t build enough homes for the last decade. Now, add the "lock-in effect" I mentioned earlier, where current homeowners refuse to sell because they’d lose their low mortgage rate, and you get a market with very few listings.

Builders are trying to fill the gap, but they face their own headwinds. Insurance markets are stressed, especially in states prone to wildfires or hurricanes. Labor is expensive. Land is scarce in desirable areas. So, while there is cautious optimism that production might tick up slightly as financial conditions ease a bit, it’s not going to be a flood of new inventory. It’s a trickle. And most of that new construction is aimed at the higher end of the market because that’s where the profit margins are.

This means buyers have to change their hunting grounds. If you’re only looking at turnkey, move-in-ready homes in popular suburbs, you’re going to be disappointed. You might need to look at homes that need cosmetic work. Paint and flooring are expensive, but they’re cheaper than a bidding war on a perfect house. Or, you might need to expand your geographic radius. Look at towns twenty minutes further out. Look at neighborhoods that haven’t "trended" yet. The inventory is there, but it’s hidden in plain sight, requiring more legwork to find.

Buyer Fatigue: When Waiting Stops Making Sense

There’s a psychological toll to this market. U.S. News & World Report’s 2026 Spring Homebuying Survey found that buyers are tired. Really tired. They’ve been waiting for costs to come down, watching rates fluctuate, and getting outbid or priced out repeatedly. This fatigue leads to two extremes: some people give up entirely and resign themselves to renting forever, while others rush into bad decisions just to "get it over with." Neither is ideal.

It’s important to acknowledge this emotional exhaustion. Buying a home is stressful enough in a normal market. In 2026, it feels like a battle against invisible forces. You might feel like you’re missing out on building equity, or that you’re throwing money away on rent. These feelings are valid. But acting out of frustration can lead to buyer’s remorse. Don’t buy a house just because you’re angry at the rental market. Buy it because the numbers work for your long-term life plan.

However, there is a flip side to this fatigue. Because many buyers have dropped out of the market, competition has softened in some segments. You might not face ten offers on a house anymore. You might actually get inspections done. You might even negotiate repairs. This is a silver lining. The frenzy of 2021-2022 is gone. In its place is a slower, more deliberate market. If you can stomach the rates, you have more power to negotiate than you did a few years ago. Use that leverage. Ask for closing cost assistance. Ask for rate buy-downs. Sellers are more motivated now than they have been in a long time.

Creative Financing and the New Playbook

Since the old playbook (save 20%, get a 3% rate, buy a suburban colonial) is broken, we need a new one. In 2026, creativity is your best asset. This isn’t about risky subprime loans; it’s about using the tools available to make the math work. One popular strategy is the "2-1 buydown," where the seller pays to lower your interest rate for the first two years. This gives you breathing room initially, allowing you to adjust to the higher payment later. With sellers sitting on properties longer, they are more willing to offer these concessions.

Another option is looking at adjustable-rate mortgages (ARMs). I know, ARMs have a bad reputation from 2008. But today’s ARMs are different. If you plan to move or refinance within five to seven years, an ARM might offer a significantly lower initial rate than a 30-year fixed. It’s a calculated risk, but for some buyers, it’s the only way to qualify for the home they need. Just make sure you understand the caps and the worst-case scenario payment.

Don’t overlook local and state programs either. Many states have expanded down payment assistance grants in response to the affordability crisis. Some offer second mortgages with no interest to help cover closing costs. These programs often have income limits, so even if you earn a decent salary, you might still qualify. It’s worth spending an hour calling your local housing authority to ask. Also, consider co-buying. Pooling resources with a sibling, friend, or parent can double your purchasing power. It requires legal agreements and clear boundaries, but it’s becoming a common solution for millennials and Gen Z buyers.

While we navigate the immediate challenges, it’s worth looking at the bigger picture. The root cause of this affordability crisis isn’t just inflation; it’s a lack of supply. As noted by various housing advocates, solving the long-term problem requires building more houses. Period. We need more density, more multifamily units, and fewer zoning restrictions that block affordable developments. This won’t help you buy a house today, but it shapes the market you’ll be selling into later.

Supporting policies that encourage construction is a civic duty for homeowners and renters alike. Attend local town halls. Vote for measures that allow for accessory dwelling units (ADUs) or modest multi-family buildings. NIMBYism (Not In My Backyard) has contributed significantly to the shortage. By opposing new development, we restrict supply and drive up prices for everyone. Changing this mindset takes time, but it’s essential for a healthy housing market in the future.

For now, though, we deal with the hand we’ve been dealt. The market in 2026 is not friendly, but it’s not impossible. It rewards preparation, flexibility, and resilience. It punishes impulsiveness and rigidity. If you can adapt your expectations—maybe a condo instead of a single-family home, maybe a fixer-upper, maybe a longer commute—you can still find a path to ownership. It just looks different than the path our parents took. And that’s okay. Different doesn’t mean worse. It just means it’s ours.

Navigating the sticky inflation impact on housing in 2026 is about more than just numbers. It’s about redefining what success looks like. It’s about understanding that a 6.3% rate isn’t a failure, it’s the current landscape. It’s about recognizing that shelter costs are keeping the Fed cautious, and that won’t change overnight. But it’s also about seeing the opportunities in the fatigue of others. The market is slower. Sellers are more open to negotiation. Creative financing is more accepted.

You don’t have to solve the entire housing crisis to buy a home. You just have to solve your own puzzle. Look at your budget honestly. Explore every assistance program available. Be willing to look where others aren’t. And remember, you’re not alone in this frustration. Millions of Americans are figuring it out, one messy, complicated, hopeful step at a time. The door isn’t closed. It’s just stuck a little. You might have to shove harder, or wiggle the handle, but it will open.