You’ve built up equity in your home. Maybe it’s been a decade of steady payments, or perhaps the market in your neighborhood has surged unexpectedly. Either way, you’re sitting on a pile of cash that’s technically yours, just locked behind drywall and foundation. It feels like free money, doesn’t it? But unlocking it isn’t as simple as turning a key. You have to choose how to borrow against it. And that choice—between a Home Equity Line of Credit (HELOC) and a traditional Home Equity Loan—is where things get tricky.

Most people think they’re just picking between two similar products. They look at the interest rate, maybe glance at the monthly payment, and sign on the dotted line. Big mistake. I’ve seen too many friends and neighbors stumble because they didn’t understand the structure of what they were signing up for. It’s not just about the rate. It’s about flexibility, risk, and how your life might change over the next five or ten years. One wrong move can turn a helpful financial tool into a stressful burden.

Let’s be honest. Banking jargon is designed to confuse. Terms like "draw period," "amortization," and "variable APR" sound important, but do they really mean anything to you when you’re trying to fix a leaky roof or pay for a wedding? Probably not. That’s why we need to strip away the noise. We’re going to look at what actually matters. Not what the bank brochure says, but what happens in real life when the bills come due. Because the difference between these two loans isn’t just math. It’s peace of mind.

The Illusion of Simplicity in Lump Sum Loans

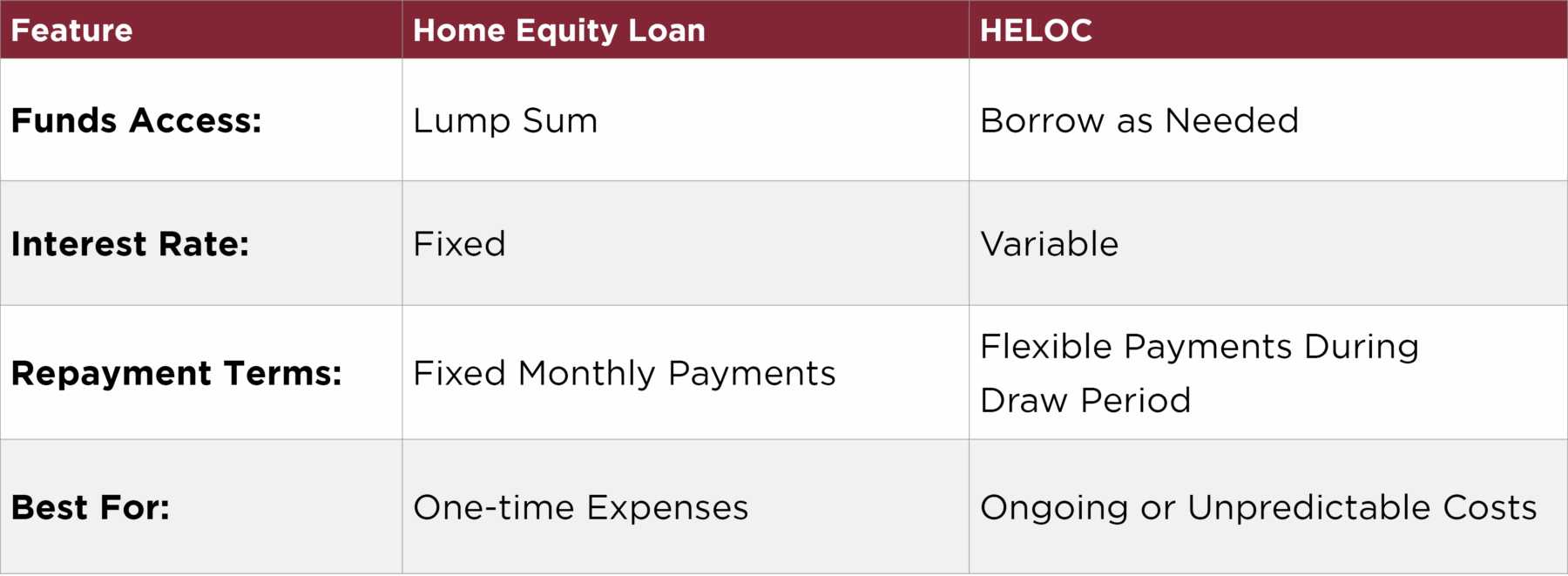

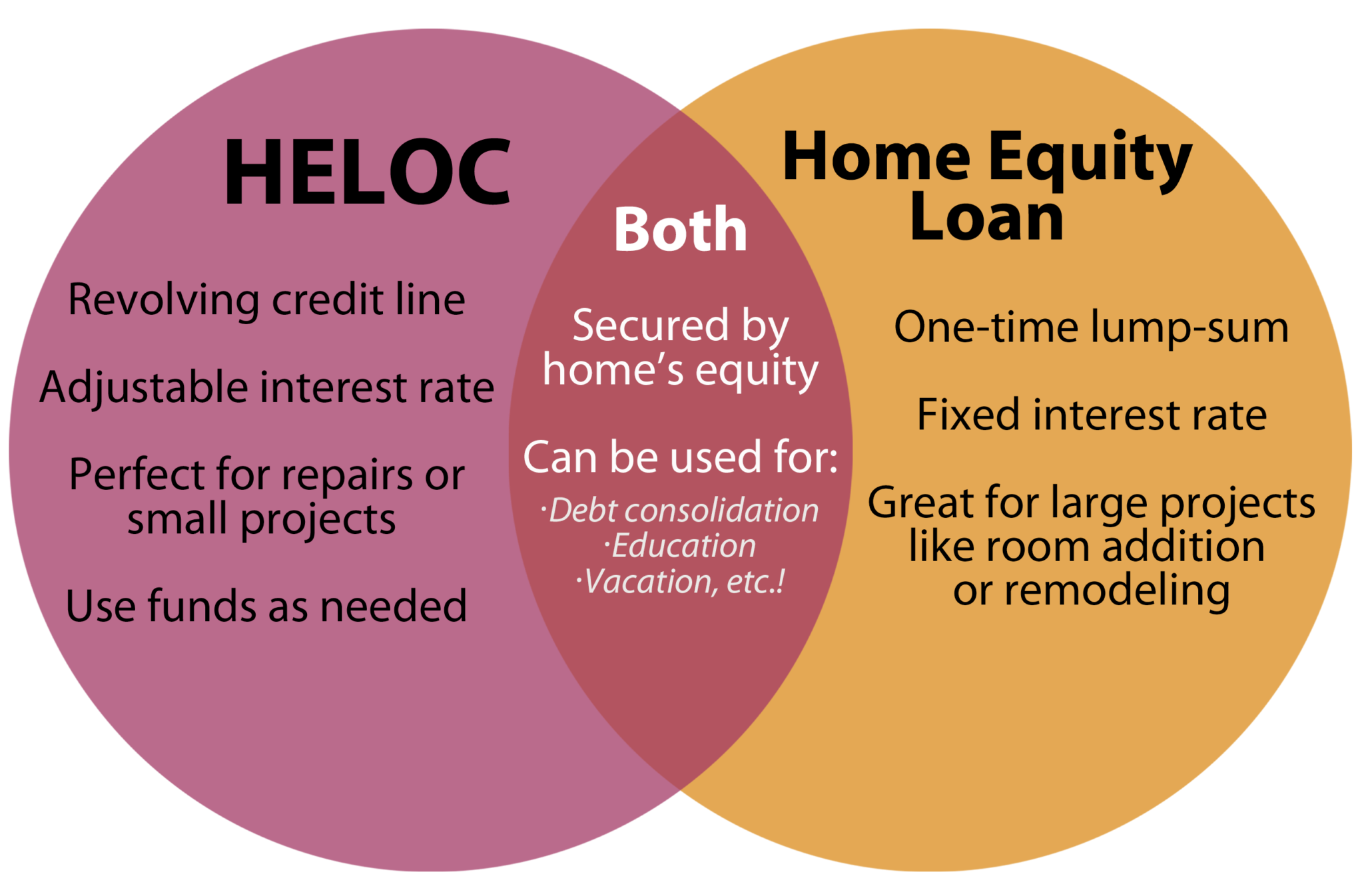

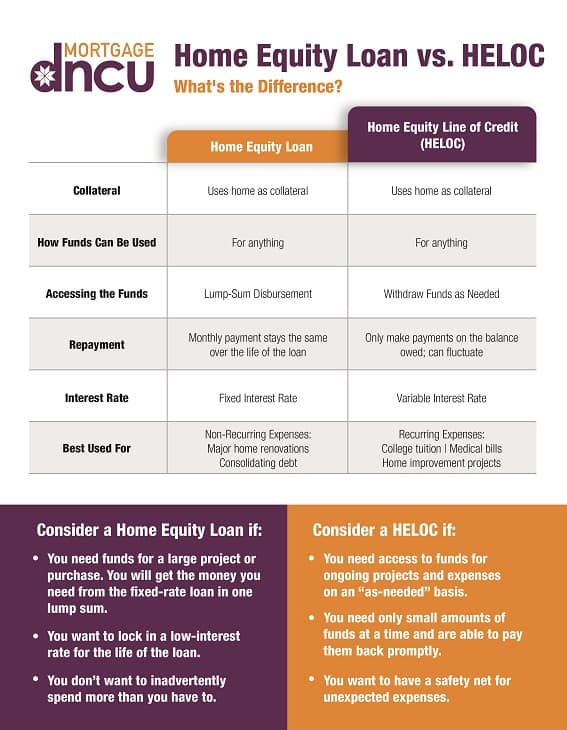

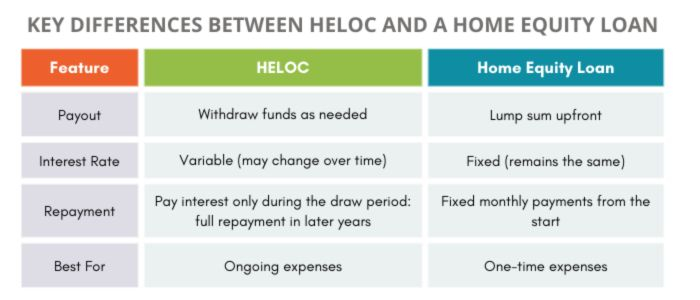

A home equity loan is often called a "second mortgage." It sounds solid. Reliable. You get a chunk of cash all at once—say, $50,000—and you pay it back in fixed monthly installments over a set term, like 10 or 15 years. The interest rate is usually fixed, too. This predictability is its biggest selling point. You know exactly what you owe every month, from day one until the day it’s paid off. For many homeowners, this feels safe. And in many cases, it is.

But here’s what people miss: the rigidity. Once you take that lump sum, you’re stuck with it. Let’s say you borrow $50,000 to remodel your kitchen. Halfway through the project, you realize you also need to replace the HVAC system. Too bad. You can’t just dip back into the loan for more money. You’d have to apply for a completely new loan, with new fees, new credit checks, and potentially a different interest rate. It’s inefficient. It’s like buying a single-use ticket when you might need a season pass.

There’s also the psychological trap of the "big check." When that $50,000 hits your account, it feels like wealth. But it’s debt. Every dollar of it. With a fixed loan, you start paying interest on the entire amount immediately, even if you only spend $10,000 in the first month. If you’re disciplined, this isn’t a problem. But humans aren’t always disciplined. That leftover cash sitting in your checking account can tempt you to spend it on things that don’t add value to your home. Suddenly, you’re paying interest on a vacation you took three years ago. Ouch.

The Flexibility Trap of the HELOC

Now let’s look at the HELOC. Think of it like a credit card, but with your house as collateral. You get approved for a limit, say $50,000, but you don’t have to take it all. You can draw $5,000 today, another $10,000 next month, and nothing for the rest of the year. You only pay interest on what you actually use. This sounds amazing, right? It’s flexible. It’s efficient. It’s perfect for ongoing projects or emergency funds.

But flexibility comes with a price tag that’s often hidden in plain sight: variable interest rates. In 2026, rates are still fluctuating based on the Federal Reserve’s moves. A HELOC’s rate is tied to an index, like the prime rate. If rates go up, your payment goes up. It’s not a maybe. It’s a guarantee. I’ve talked to homeowners who started with a comfortable $300 monthly payment during the draw period, only to see it jump to $600 or more when rates climbed. That shock can wreck a monthly budget.

And then there’s the "draw period" confusion. Most HELOCs have a 10-year draw period where you can borrow and repay freely. After that, you enter the "repayment period," which can last another 10 to 20 years. During repayment, you can no longer borrow. You just pay back what’s left. Here’s the kicker: some loans require you to pay off the entire balance at the end of the draw period, or refinance. If you haven’t planned for that balloon payment or refinancing hurdle, you could be stuck. It’s a complex dance, and many people don’t realize they’re signing up for it until the music stops.

The Rate Risk Nobody Talks About

We’ve touched on rates, but let’s dig deeper. When you compare a home equity loan and a HELOC side-by-side, the initial rate on the HELOC often looks lower. It’s tempting. "Look, I can save half a percent!" you think. But that’s a snapshot, not a movie. A home equity loan locks in your rate. If market rates soar in 2027 or 2028, you’re smiling. Your payment stays the same. You’re insulated.

With a HELOC, you’re exposed. Every time the Fed raises rates, your cost of borrowing increases. In a high-inflation environment, this can add thousands of dollars to your total cost over the life of the loan. Sure, if rates drop, you benefit. But can you bet your financial stability on rates dropping? Most financial advisors say no. They call it "interest rate risk." I call it losing sleep.

Consider this scenario: You take out a $40,000 HELOC at a variable rate of 7%. Your initial payment is manageable. Two years later, rates rise by 2%. Your payment jumps. You adjust. Then rates rise another 1.5%. Now you’re stretched thin. Meanwhile, your neighbor took a fixed-rate home equity loan at 8%. Their payment never changed. They planned their budget around that number. Who’s in a better position? The person with the predictable cost, almost every time. Unless you’re certain rates will fall, the fixed rate offers a shield that the variable rate simply can’t match.

Timing Your Needs vs. Timing the Market

One of the most overlooked factors is when you need the money. This seems obvious, but it’s where people mess up. If you have a single, defined expense—like a $30,000 roof replacement or a $25,000 debt consolidation—you know exactly how much you need. You need it all at once. In this case, a home equity loan is usually the better fit. You get the cash, you pay the contractor, you start repaying. Clean. Simple. Done.

But what if your needs are fuzzy? Maybe you’re planning a multi-year renovation. First, the basement this year. Then the bathroom next year. Or maybe you want a safety net for medical emergencies or job loss. You don’t know how much you’ll need, or when. A HELOC shines here. You keep the line open. You draw only when necessary. You repay as you can. It’s a financial cushion that grows and shrinks with your life.

The mistake? Using a HELOC for a one-time expense. Why? Because you’re taking on variable rate risk for no reason. If you know you need $20,000 today, just take the fixed loan. Don’t leave the door open to rate hikes. Conversely, using a fixed loan for ongoing needs is wasteful. You’ll pay interest on money you haven’t spent yet. Match the tool to the task. It’s like using a screwdriver for a screw and a hammer for a nail. Seems basic, but you’d be surprised how many people try to hammer a screw.

The Hidden Fees and Closing Costs

Let’s talk about the stuff banks don’t highlight in big bold font: fees. Both HELOCs and home equity loans come with closing costs. These can include appraisal fees, application fees, origination fees, and title search costs. In some cases, these can run 2% to 5% of the loan amount. On a $50,000 loan, that’s $1,000 to $2,500 just to get started.

Here’s the twist: many lenders offer "no-closing-cost" HELOCs. Sounds great, right? But there’s no such thing as a free lunch. Usually, they waive the upfront fees but charge a higher interest rate, or they add an "annual fee" or "maintenance fee" to keep the line open. Or, if you close the HELOC within the first few years, they hit you with an "early closure fee." It’s a trap for the unwary. You think you’re saving money upfront, but you’re paying more over time.

Home equity loans, on the other hand, often have more transparent fee structures. You pay the closing costs upfront, and that’s it. No surprise annual fees. No penalties for paying it off early (usually). But you need to read the fine print. Some lenders charge prepayment penalties on fixed loans too. Always ask: "What does it cost to get this loan? What does it cost to keep it? And what does it cost to get rid of it?" If the loan officer hesitates, walk away. Transparency is your best friend.

Finally, let’s address the elephant in the room: your home is on the line. Both HELOCs and home equity loans are secured by your house. If you stop paying, the lender can foreclose. This isn’t a credit card debt where your credit score takes a hit. This is your roof. Your sanctuary. Your family’s home.

This reality changes how you should approach the decision. A HELOC’s flexibility can encourage casual borrowing. "I’ll just pull out $5,000 for a trip. I’ll pay it back quickly." But life happens. Jobs get lost. Medical bills pile up. That $5,000 turns into $15,000, and the variable rate keeps climbing. Suddenly, the debt feels unmanageable. The stress isn’t just financial; it’s existential. You’re risking your home for a vacation.

A fixed home equity loan forces discipline. You borrow a set amount. You have a plan. You repay it on a schedule. It’s harder to misuse. It creates a boundary. For many people, this structure provides emotional security. They know exactly when they’ll be debt-free. They can visualize the finish line. With a HELOC, the finish line moves. It’s a revolving door. For some, that’s liberating. For others, it’s a source of constant anxiety. Know yourself. Are you a disciplinarian or a dreamer? Choose the loan that matches your personality, not just your wallet.

Choosing between a HELOC and a home equity loan isn’t just a math problem. It’s a life problem. It’s about predicting your future needs, managing risk, and understanding your own habits. There’s no "better" option. There’s only the right option for you, right now. Take your time. Ask the hard questions. Read the fine print. And remember, your home is more than an asset. It’s your foundation. Treat it with care.