Losing someone is hard enough without having to navigate a maze of tax codes and financial jargon. But here you are, staring at a stack of paperwork, wondering what it all means for your wallet. It’s overwhelming. I get it. One of the most confusing parts? Figuring out what you actually "paid" for the house, stocks, or land you just inherited. This number is called your cost basis, and getting it wrong can cost you thousands later on.

The good news is that the IRS has a rule designed to help heirs, not hurt them. It’s called the "step-up in basis." In plain English, it means the value of what you inherit gets reset to what it’s worth today, not what your loved one paid for it decades ago. This little tweak can save you a fortune in capital gains taxes. Let’s break it down so you can breathe easier and make smart moves with your new assets.

What Exactly Is Cost Basis?

Think of cost basis as your starting line for taxes. When you buy something—like a share of stock or a vacation cabin—the price you pay is your basis. If you sell it later for more than that price, you owe taxes on the profit, known as capital gains. Simple enough, right? But when inheritance enters the picture, the rules change completely. You didn’t buy the asset; it was given to you through a will or trust. So, what’s your starting line?

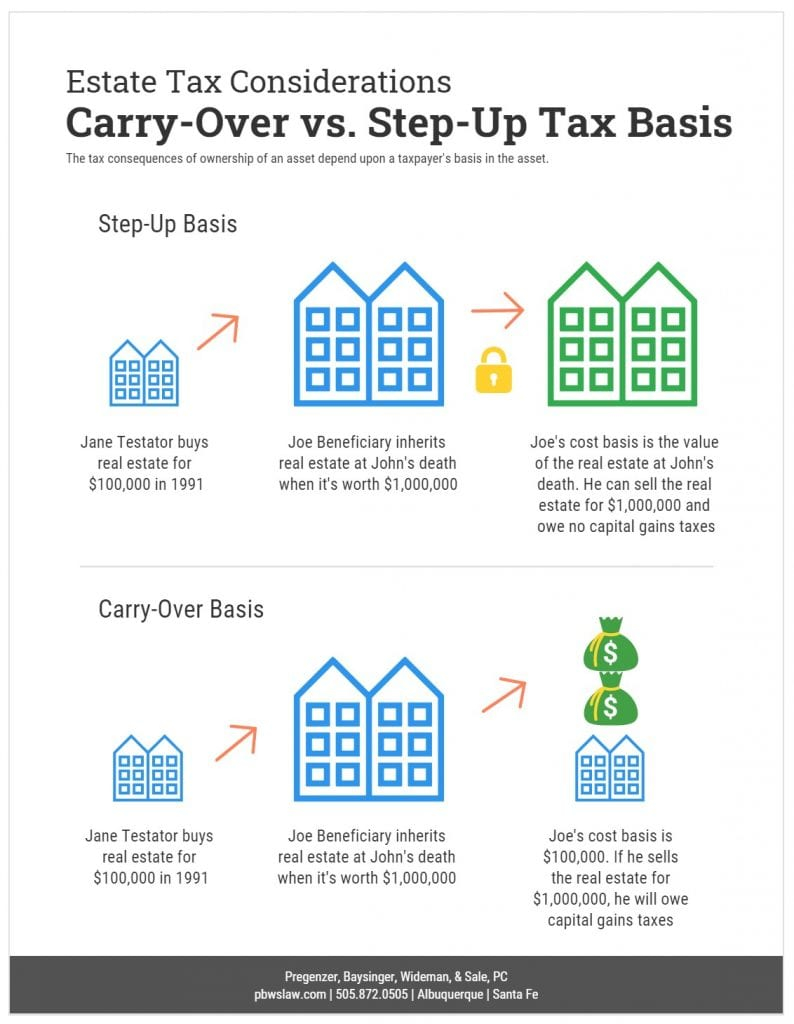

For inherited items, the IRS doesn’t care about the original purchase price. Instead, they look at the fair market value (FMV) on the date the person passed away. This is the magic moment where the old basis disappears and a new one takes its place. If your grandfather bought a plot of land for $10,000 in 1980, but it’s worth $500,000 when he dies in 2026, your new cost basis is $500,000. That huge jump in value that happened over 40 years? It basically vanishes for tax purposes.

This concept is crucial because it determines how much tax you’ll pay if you decide to sell. Without this reset, you’d be on the hook for taxes on all that growth since 1980. With the step-up, you only pay taxes on any increase in value after the date of death. It’s a massive difference. And honestly, it’s one of the few silver linings in the tax code for grieving families.

The Magic of the Step-Up in Basis

So, how does this "step-up" actually work in practice? Let’s use a real-world example. Imagine your aunt leaves you her home. She bought it in 1995 for $150,000. Over the years, the neighborhood got trendy, schools improved, and the market boomed. By the time she passes in early 2026, an appraisal shows the home is worth $600,000.

If you sell the house immediately for $600,000, your cost basis is $600,000. Your profit is zero. You owe $0 in capital gains tax. Pretty sweet deal, huh? Now, let’s say you decide to keep the house for a few years. The market keeps climbing. In 2028, you sell it for $650,000. Your gain is only $50,000 ($650,000 sale price minus $600,000 stepped-up basis). You only pay taxes on that $50k, not the $500k gain that happened while your aunt owned it.

It’s important to note that this isn’t always a "step-up." Sometimes, values drop. If the asset is worth less on the date of death than what the original owner paid, your basis "steps down" to that lower value. This is rare for real estate in recent years, but it happens with stocks or volatile investments. The rule is symmetrical: your basis becomes the FMV at death, whether that’s higher or lower than the original cost. Most of the time though, we’re talking about a step-up, which is why everyone talks about it so much.

Why the Date of Death Matters So Much

You might be wondering, "How do we prove what the house was worth on that specific day?" Great question. The IRS requires documentation. You can’t just guess. For real estate, this usually means getting a professional appraisal dated as close to the date of death as possible. Some people use a comparative market analysis from a realtor, but an appraisal is safer and more defensible if the IRS ever comes knocking.

For stocks and bonds, it’s easier. You just look up the closing price on the date of death. If the market was closed (like on a weekend), you use the next trading day. Many brokerage firms will even provide a statement showing the value of inherited assets on the date of death, which saves you a lot of headache. Keep these records safe. You’ll need them when you file your taxes after you eventually sell.

There’s also something called the "alternate valuation date." Executors of an estate can choose to value assets six months after the date of death instead. Why would they do that? Usually, if the overall value of the estate has dropped significantly in those six months, this can lower estate taxes. But be careful: if they choose this option, your cost basis is also based on that six-month-later value, not the date of death. It’s a trade-off. Talk to a tax pro if this applies to you, because it can get complicated fast.

Different Assets, Different Rules

Not everything gets a full step-up. Most things do, like houses, stocks, mutual funds, and family heirlooms. But there are exceptions. For instance, if you inherit an IRA or a 401(k), those don’t get a step-up in basis. They are considered "income in respect of a decedent." You’ll still owe income tax when you withdraw the money, just like the original owner would have. This is a big trap for unsuspecting heirs. Don’t assume your inherited retirement account is tax-free. It’s not.

Another tricky area is joint ownership. If you owned a house jointly with your spouse, and one of you passes away, the rules depend on where you live. In community property states (like California, Texas, and Arizona), the entire property often gets a step-up in basis. In common law states, usually only half of the property gets the step-up—the half owned by the deceased. This distinction can mean a huge difference in taxes if you sell later.

What about gifts? If your loved one gave you the property before they died, you don’t get a step-up. You take their original cost basis. This is called a "carryover basis." So, if they bought stock for $10 and it’s worth $100 when they gift it to you, your basis is $10. If you sell it for $100, you owe taxes on $90 of gain. If they had waited and left it to you in their will, your basis would be $100, and you’d owe nothing. Timing matters immensely.

Common Mistakes Heirs Make

One of the biggest errors people make is assuming they don’t need to track the basis because they didn’t "buy" anything. Wrong. You absolutely need to know your basis. When you sell, you’ll report the sale on Schedule D of your tax return. If you don’t have a recorded basis, the IRS might assume it’s zero. That means you’d pay taxes on the entire sale price. Ouch. Always get that appraisal or statement.

Another mistake is mixing up inheritance tax and capital gains tax. Inheritance tax is paid by the estate (or sometimes the heir) to the state, and only a few states have it. Capital gains tax is federal (and sometimes state) and is paid by you when you sell the asset. The step-up in basis helps with capital gains, not necessarily inheritance tax. Don’t confuse the two. They are separate beasts.

Also, watch out for improvements. If you inherit a fixer-upper and spend $50,000 renovating it before selling, you can add that $50,000 to your stepped-up basis. So if your basis was $600,000 and you spent $50k on a new roof and kitchen, your new basis is $650,000. This lowers your taxable gain further. Keep every receipt. Every single one. It adds up.

Planning Ahead for Your Heirs

If you’re the one leaving assets behind, think about how this affects your kids. Sometimes, people try to "help" by putting their name on the deed or gifting assets early to avoid probate. But as we discussed, this strips away the step-up in basis. It might save on probate fees, but it could create a massive tax bill for your heirs. Often, letting the asset pass through the will or trust is the smarter tax move.

Consider talking to an estate planner. They can help you structure your assets to maximize the step-up benefit. For example, they might advise against gifting highly appreciated stock. Or they might suggest certain trusts that preserve the step-up. It’s not just about who gets what; it’s about how much they keep after taxes. A little planning now can save your family a lot of stress and money later.

And remember, laws can change. While the step-up in basis has been a cornerstone of US tax law for a long time, politicians occasionally propose changing or eliminating it. As of 2026, it’s still here, but it’s always wise to stay informed. Check with a tax advisor every few years to make sure your estate plan still makes sense under current laws. Don’t set it and forget it.

Inheriting property is emotional, complex, and frankly, a bit of a logistical nightmare. But understanding cost basis doesn’t have to be. Remember the golden rule: your basis is generally the fair market value on the date of death. This step-up wipes out years of capital gains, saving you from a hefty tax bill. Get an appraisal. Keep good records. And don’t rush to sell unless you’re ready.

Take a breath. You don’t have to figure this all out overnight. Gather your documents, talk to a professional if things feel shaky, and give yourself grace. Grieving takes time, and so does sorting out an estate. By knowing how the step-up works, you’re already ahead of the game. You’re protecting your future self from unnecessary taxes and headaches. And that’s a win, even on a tough day.