You know that feeling when you’re staring at a spreadsheet, and the numbers just start to blur together? That’s exactly where a lot of investors found themselves heading into this year. The market has been a bit of a rollercoaster, hasn’t it? One minute everyone is panicking about rising rates, and the next, there’s this quiet confidence creeping back in. If you’ve been trying to make sense of the capitalization rate shifts happening across major US cities in 2026, you aren’t alone. It’s confusing. But here’s the thing: once you stop looking at cap rates as just dry percentages and start seeing them as a story about risk and reward, everything clicks.

We are standing at a pretty interesting crossroads right now. Recent data from big players like CBRE and Colliers suggests we aren’t just drifting anymore; we are entering a new cycle. For the first time in a while, the fog is lifting. Pricing is becoming clearer. The bid-ask spreads—those annoying gaps between what sellers want and what buyers will pay—are finally narrowing. This article isn’t about throwing complex formulas at you. It’s about giving you the lens to see what’s actually happening on the ground in markets from Austin to Boston. Let’s dig in.

The Big Picture: Are Rates Rising or Falling?

So, what’s the verdict? Are cap rates going up or down in 2026? Well, if you ask ten different brokers, you might get eleven answers. But if you look at the broader surveys, a pattern emerges. The latest CBRE Cap Rate Survey, now in its 17th year, hints that we are moving into a new phase. We are seeing falling cap rates in many sectors, which usually signals growing investor confidence. When people feel good about the future, they are willing to pay more for the same income stream, which pushes the cap rate down. It’s a sign that the fear from the previous years is fading.

However, it’s not a uniform drop across the board. That’s a common mistake beginners make—assuming the whole country moves in lockstep. It doesn’t. Matthews Commercial recently pointed out that there is a widening dispersion. What does that mean? It means the gap between the "safe" assets and the "risky" ones is getting bigger. Investors are being picky. They aren’t just buying any old building; they are scrutinizing asset-specific risks. So, while the median might be stabilizing or dipping slightly, the reality on the street is much more nuanced. You have to look closer.

This divergence is actually good news for savvy buyers. Why? Because it creates opportunity. In a market where everything is priced the same, there’s no room for negotiation or finding hidden gems. But now? Now you can find deals if you know where to look. The transaction activity is expected to improve throughout 2026 precisely because this pricing clarity is returning. People know what things are worth again. That certainty brings liquidity back into the system, which is the lifeblood of real estate investing.

Regional Winners and Losers in 2026

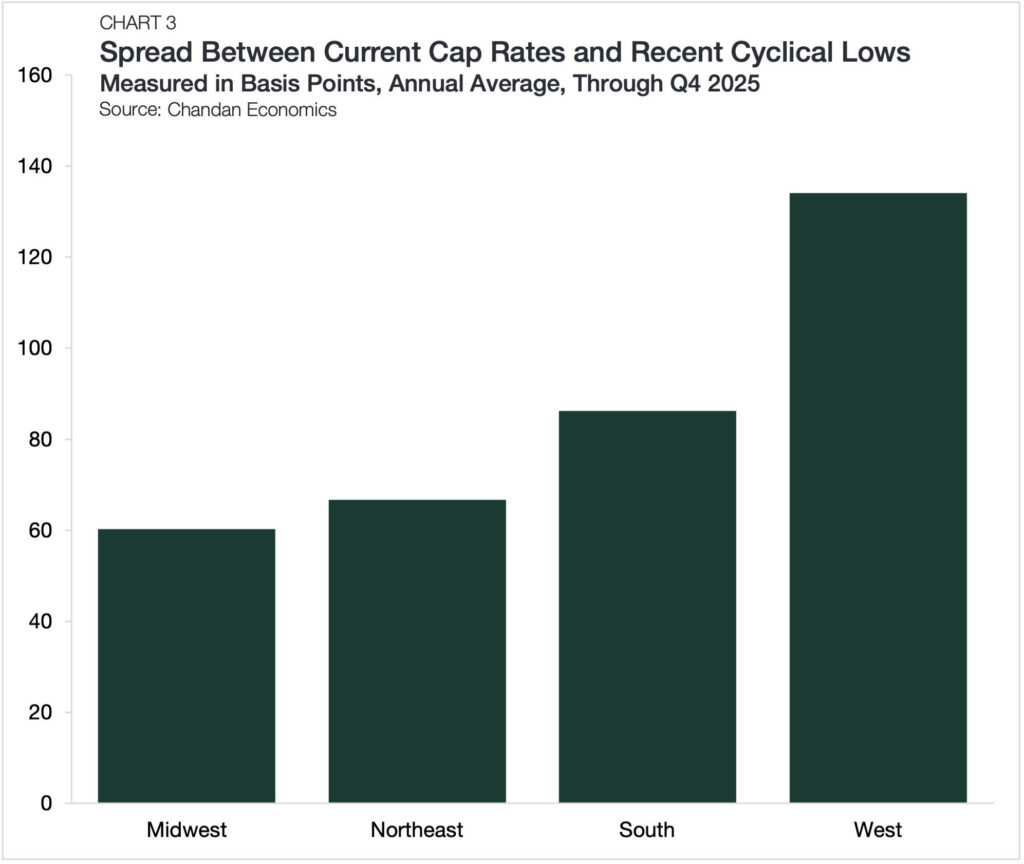

Let’s talk geography. Where is the action? If you look at data covering 775 US cities, like the reports from CapRateCity, you see some stark contrasts. The Sun Belt markets, which saw explosive growth a few years ago, are cooling off in terms of price appreciation, but their cap rates remain attractive compared to the coasts. Cities like Atlanta, Dallas, and Phoenix are offering yields that just don’t exist in New York or San Francisco anymore. For an investor looking for cash flow, these regions are still shouting loud and clear.

On the flip side, the gateway cities are seeing cap rates compress, or shrink. Why? Because institutional money loves safety. When uncertainty looms, big funds park their cash in stable, high-barrier-to-entry markets. So, while you might get a 4% cap rate in Manhattan, you might get 6.5% or higher in secondary markets. It’s a trade-off. Do you want lower yield with potentially higher long-term appreciation and stability? Or do you want higher immediate cash flow with a bit more volatility? There is no wrong answer, only the right answer for your specific goals.

Don’t ignore the Midwest either. Markets like Chicago and Minneapolis are often overlooked, but they offer a balance that is hard to beat. The cap rates here are steady, not swinging wildly like in some hype-driven markets. Newmark’s recent valuation survey highlighted that these mature markets are seeing consistent demand, especially for well-located assets. It’s boring, sure. But in real estate, boring often pays the bills. The key is to match the regional trend with your exit strategy. If you plan to hold for ten years, the current cap rate matters less than the job growth and population trends in that city.

Sector-Specific Trends: Not All Properties Are Equal

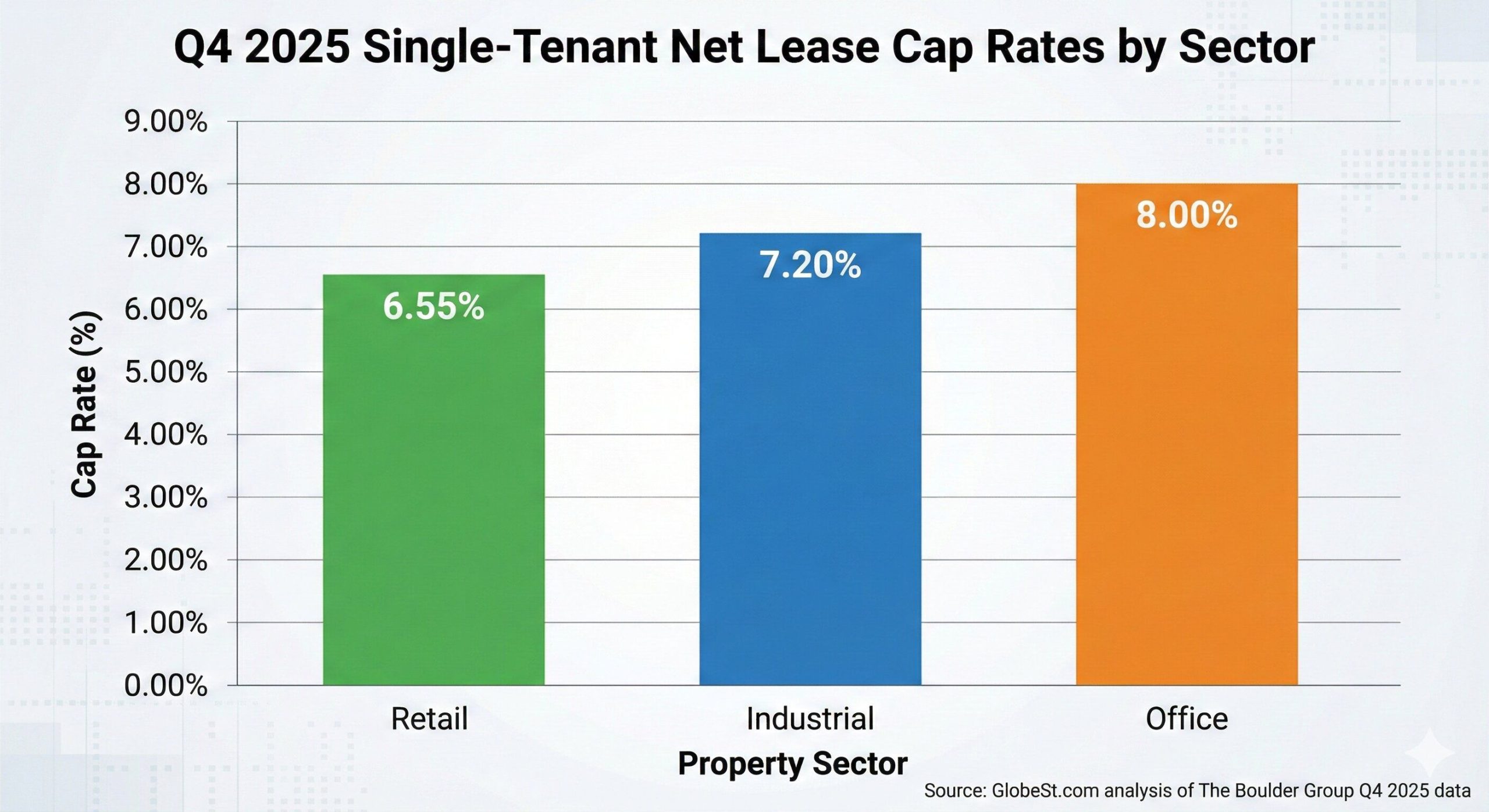

Here is a truth that saves investors from disaster: property type matters more than ever in 2026. You can’t just say "I’m buying commercial real estate." You have to specify what kind. The data from Commercial Loan Direct and others shows a massive split. Multifamily properties, especially those in areas with strong job growth, are holding their value well. Why? Because people always need a place to live. Even with remote work trends settling in, the demand for quality rental housing hasn’t vanished. Cap rates here are relatively stable, reflecting that durable demand.

Industrial real estate is another interesting beast. It’s not the gold rush it was in 2021, but select industrial assets—like last-mile delivery hubs near major cities—are still commanding premium prices (and thus lower cap rates). However, older, Class B industrial warehouses in less strategic locations are seeing upward pressure on cap rates. Buyers are wary of obsolete buildings. Similarly, grocery-anchored retail is performing surprisingly well. It’s considered "necessity-based," meaning people buy food regardless of the economy. These assets are seeing cap rates hold steady or even compress slightly as investors chase safety.

Then there is the elephant in the room: Office space. Let’s be honest, it’s struggling. Cap rates for office properties are under significant upward pressure, meaning prices are dropping to compensate for the higher perceived risk. Vacancy rates are still high in many downtown cores, and lease rollover risk is real. If you are looking at office deals in 2026, you need a very high cap rate to justify the headache. It’s a buyer’s market, but only if you have the expertise to reposition the asset. For most everyday investors, staying away from office unless you have a solid value-add plan is probably the wise move.

The Financing Connection: DSCR and Your Bottom Line

You can’t talk about cap rates without talking about loans. They are two sides of the same coin. In 2026, lenders are still strict. Most require a Debt Service Coverage Ratio (DSCR) of 1.0 to 1.25. What does that mean for you? It means your property’s net operating income needs to be 25% higher than your mortgage payment, at minimum. Here is the kicker: higher cap rate markets give you more breathing room to hit that ratio. If you are buying in a low cap rate market like Los Angeles, your cash flow might be thin, making it harder to qualify for a loan unless you put a huge down payment.

HonestCasa’s recent analysis on DSCR cap rates highlights this dynamic perfectly. In markets with higher cap rates, the income generated by the property is larger relative to the purchase price. This makes it easier to satisfy lender requirements. So, if you are leveraging your investment (using a loan), you might actually find it easier to deploy capital in secondary markets with higher yields than in prime coastal cities. It’s counterintuitive. We often think "prime location" equals "easier financing," but in today’s rate environment, cash flow is king. Lenders want to see that the property can pay for itself.

This also means you need to run your numbers with current interest rates, not the ones from three years ago. A property that looked great at a 3% interest rate might be a cash-flow negative disaster at 7%. Always stress-test your deal. Assume rates might go up slightly or vacancies might rise. If the deal still works with a conservative DSCR buffer, then you’ve got something solid. Don’t let a flashy low cap rate blind you to the financing hurdles you’ll face at closing.

Reading Between the Lines: Risk and Dispersion

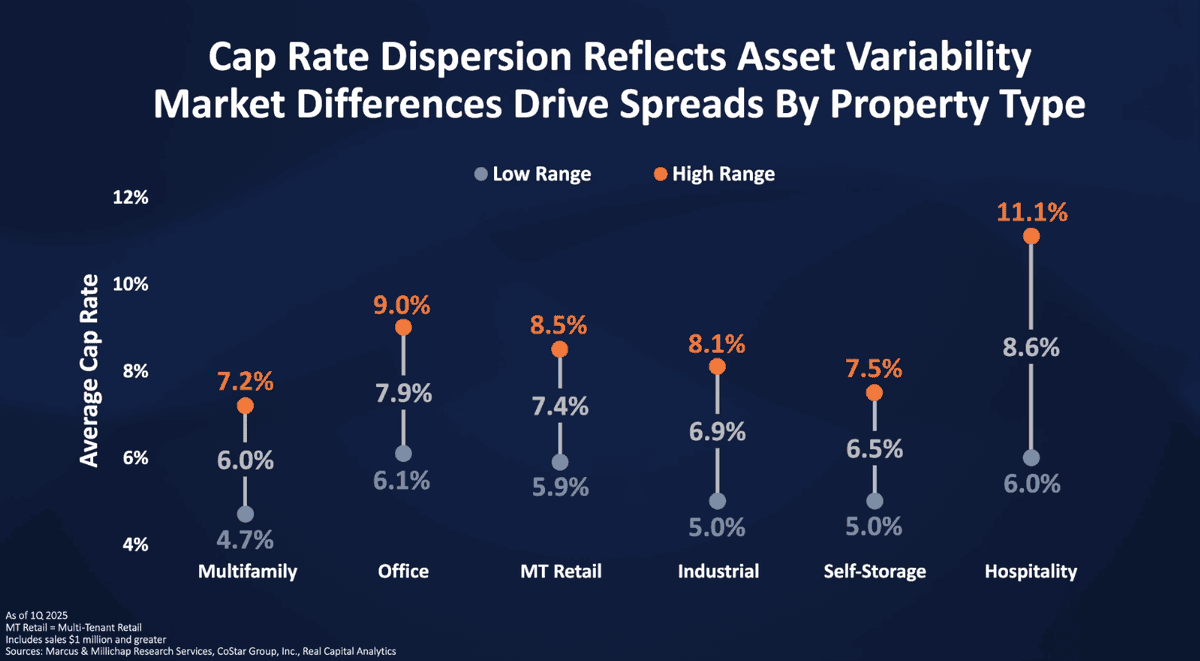

One of the most important skills in 2026 is understanding risk dispersion. As mentioned earlier, the gap between the best and worst assets is widening. This isn’t just about location; it’s about quality. A Class A multifamily building in a growing suburb might have a cap rate of 5%, while a Class C building in the same city might trade at 7%. That 2% difference isn’t arbitrary. It reflects the cost of repairs, the likelihood of tenant turnover, and the potential for rent growth. In the past, investors might have chased the higher cap rate without looking at the work involved. Today, that’s a recipe for losing money.

Matthews Commercial noted that pricing is increasingly reflective of asset-specific risk. This means you can’t rely on broad sector trends anymore. You have to look at the individual building. Does it have deferred maintenance? Is it reliant on a single tenant? These factors are driving cap rates up for risky assets and down for safe ones. This is actually a healthy market correction. It forces investors to do their due diligence. It rewards those who understand the physical and operational realities of their properties.

So, how do you read this? Look for the "why" behind the number. If a property has a high cap rate, ask yourself: What is the market punishing? Is it the location? The condition? The lease structure? If you can fix the problem, you might be able to capture that spread. But if the risk is structural—like a declining neighborhood—you might be catching a falling knife. Conversely, if a property has a low cap rate, ensure it’s truly low-risk. Don’t overpay for "safety" if the building is outdated and facing major capital expenditures soon.

Okay, so what do you actually do with all this information? First, stop trying to time the absolute bottom. It’s impossible. Instead, focus on finding deals that make sense at today’s prices. With transaction activity improving in 2026, there are more opportunities coming to market. Use the narrowing bid-ask spreads to your advantage. Sellers are becoming more realistic. Don’t be afraid to negotiate, but be ready to move quickly when you find a property that meets your criteria. Hesitation costs money in a recovering market.

Second, diversify your approach. Don’t put all your eggs in one basket. Consider mixing stable, lower-yield assets in gateway cities with higher-yield plays in growing secondary markets. This balances your portfolio. You get the stability of the big markets and the cash flow boost from the smaller ones. Also, keep an eye on insurance costs. Wexford Insurance pointed out that commercial property insurance is a major factor in 2026 profitability. A high cap rate might look great until you realize the insurance premiums have doubled due to climate risk in that area. Always factor in total operating expenses, not just the mortgage.

Finally, build relationships with local brokers. In a market with wide dispersion, off-market deals and insider knowledge are invaluable. Brokers know which sellers are motivated and which properties have hidden issues. They can help you interpret the local cap rate trends that national reports might miss. Remember, real estate is a local game. National trends give you context, but local knowledge gives you the edge. Stay curious, stay cautious, and keep your eyes on the long-term fundamentals of the communities you invest in.

Navigating the 2026 cap rate landscape doesn’t have to be overwhelming. It’s about shifting your mindset from chasing simple percentages to understanding the story behind the numbers. The market is maturing, becoming more rational, and offering clear signals if you know how to read them. Whether you are drawn to the stability of multifamily in the Northeast or the cash flow potential of industrial in the South, the opportunities are there. They just require a bit more homework than before.

The key takeaway? Don’t fear the complexity. Embrace it. The widening dispersion and sector-specific trends mean that generic strategies won’t work as well as they used to. Success this year belongs to the investors who dig deeper, who question the assumptions, and who align their purchases with their actual financial goals and risk tolerance. Keep your calculations conservative, your eyes open for local nuances, and your focus on long-term value rather than short-term speculation.

Real estate has always been a marathon, not a sprint. The fluctuations of 2026 are just one leg of that race. By understanding how cap rates are behaving now, you are positioning yourself not just to survive the current cycle, but to thrive in the next one. So take a breath, look at the data with fresh eyes, and remember that every number on that spreadsheet represents a real building, with real tenants, in a real community. Treat it with that respect, and the returns will follow.