You’ve probably heard the rumors. Maybe a friend mentioned they bought a house with literally zero money down. Or perhaps you saw a listing online that seemed too good to be true, tucked away in a quiet neighborhood just outside the city limits. It’s not a scam. It’s not a glitch in the matrix. It’s the USDA loan program, and in 2026, it remains one of the most powerful, yet underutilized, tools for homebuyers and investors alike.

But here’s the catch: you can’t just buy any house. You have to be in the right spot. That’s where the map comes in. For years, people assumed "rural" meant miles from civilization, surrounded by cornfields and silence. That’s outdated thinking. Today, the definition of eligible areas has shifted, expanded, and in some cases, surprised even seasoned real estate agents. If you’re looking to buy in 2026, understanding this map isn’t just helpful—it’s essential. It’s the difference between scraping together a 20% down payment or keeping that cash in your pocket for renovations, emergencies, or just breathing easier.

So, how do you actually read this thing? And more importantly, how do you know if your dream home qualifies? Let’s dive into the details, strip away the jargon, and look at what the 2026 landscape really looks like for anyone hoping to leverage these federal benefits.

Decoding the Green Zones: What the Map Actually Shows

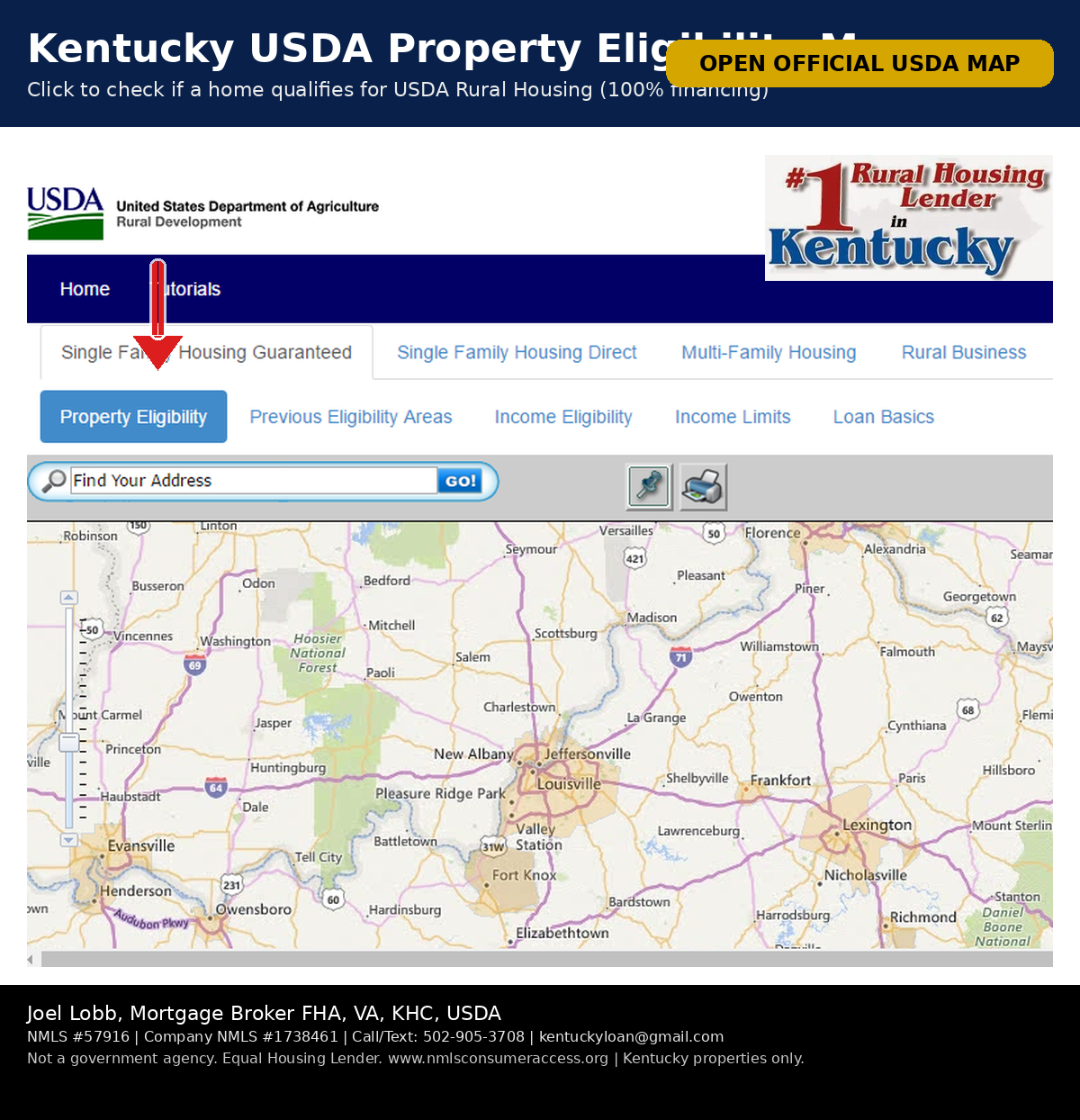

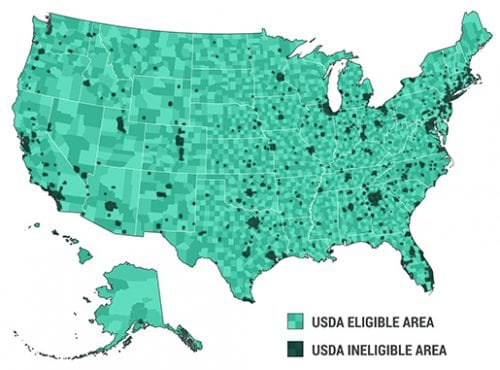

When you first pull up the official USDA eligibility site, it can feel a bit overwhelming. There are lines, colors, and tiny text boxes everywhere. But once you know what you’re looking for, it becomes surprisingly simple. The core of the system is color-coded. Generally, areas that qualify for USDA financing show up in green or are marked as qualifying zones. These are the "go" signals. If a property sits within these boundaries, it meets the geographic requirement for a Rural Development loan.

It’s important to note that the map isn’t static. The USDA updates it regularly to reflect population changes and urban sprawl. As of May 2026, the map has been revised to ensure it remains current through the end of the year. This means some areas that were ineligible last year might now be open, while others on the fringe of growing cities might have slipped off the list. The system makes every effort to provide accurate info, but there’s a disclaimer you should always keep in mind: the USDA doesn’t guarantee the absolute accuracy of every pixel. Final determination always rests with the lender and the specific property appraisal. So, while the map is your best starting point, it’s not the final word.

Think of the map as a filter, not a guarantee. It tells you where you can look, not necessarily what you will get. Many buyers make the mistake of falling in love with a home only to realize later it sits in a red (ineligible) zone. Save yourself the heartache. Before you schedule a viewing, plug the address into the eligibility tool. It takes seconds and can save you weeks of wasted time. The interface on sites like eligibility.sc.egov.usda.gov is designed for this exact purpose—quick, instant checks that give you a clear yes or no on location.

Beyond the Cornfields: Surprising Suburban Eligibility

Here’s the biggest misconception about USDA loans: that you have to live in the middle of nowhere. That’s simply not true in 2026. In fact, a huge portion of eligible properties are in what we’d normally call suburbs. As cities expand, the "rural" designation often extends further out than people expect. You might be looking at a nice subdivision with paved streets, streetlights, and a nearby grocery store, and still qualify for a zero-down loan.

Sources like Mortgage-info and Amerisave have highlighted this trend repeatedly. Many homebuyers are shocked to find that their desired neighborhood, just 15 or 20 minutes from the city center, is fully eligible. This opens up a world of opportunities for families who want the convenience of suburban life without the barrier of a massive down payment. It’s not just for farmers or remote workers anymore. It’s for teachers, nurses, IT professionals, and anyone else looking to buy their first home in a community that feels connected but still retains that "rural" character defined by population density rather than isolation.

This shift is crucial for investors too. If you’re looking to buy rental properties, the eligible zones often include areas with strong rental demand due to their proximity to urban job centers. You get the benefit of low-interest, government-backed financing in areas that appreciate steadily because they’re desirable places to live. Don’t assume a place is ineligible just because it has a Starbucks nearby. Check the map. You’d be surprised how many "suburban" pockets remain green. It’s a game-changer for building wealth through real estate without tying up all your liquid cash upfront.

The Money Talk: Income Limits and Financial Rules

Location is only half the battle. The other half is your wallet. Specifically, how much money flows into it. USDA loans aren’t for everyone; they’re designed for low-to-moderate income households. In 2026, the income limits have been adjusted to reflect inflation and regional cost-of-living differences. For many areas, the standard limit hovers around $119,850 for a household of one to four people, though this can vary significantly by county. High-cost areas might have higher caps, while more affordable regions stick to the baseline.

Why does this matter? Because even if the house is in a green zone, you won’t qualify if your income exceeds the limit for that specific area. The USDA calculates this based on your gross annual income, including wages, bonuses, and other steady sources. It’s not just about your credit score (though that matters too); it’s about ensuring the program helps those who need it most. If you’re earning six figures in a major metro’s suburb, you might be priced out of the program. But for many middle-class families, these limits are perfectly attainable.

There’s also the credit aspect. While USDA loans are known for being flexible, they aren’t lax. You generally need a credit score of at least 640 to qualify for automated underwriting, though some lenders may go lower with manual underwriting. The beauty here is the zero-down payment feature. Unlike FHA loans which require 3.5% down, or conventional loans needing 5-20%, USDA asks for nothing upfront for the purchase price. This makes homeownership accessible to people who have good income but haven’t had the chance to save a large nest egg. It’s a lifeline for first-time buyers who are tired of renting.

How to Use the Map: A Step-by-Step Guide

Using the map is easier than you think, but doing it right saves headaches. Start by visiting the official USDA eligibility site or a trusted lender’s portal like CrossCountry Mortgage or Rocket Mortgage. These platforms often have user-friendly interfaces that simplify the process. Don’t rely on third-party blogs alone; go to the source or a reputable financial institution that updates their data daily. Once you’re there, you’ll see a search bar. Enter the specific address of the property you’re interested in. Not just the city, but the full street address. Precision matters.

If you don’t have a specific house in mind, you can browse by county or zip code. Zoom in on the map to see the boundaries. Look for the green shading. If the address falls within the green, you’re geographically eligible. If it’s in a white or red area, it’s likely ineligible. But wait—don’t give up immediately. Sometimes, the boundary lines are weird. A house on one side of the street qualifies, while the one directly across doesn’t. It’s arbitrary, but it’s the rule. Always double-check multiple addresses in your target neighborhood to get a feel for the layout.

Once you confirm the location, the next step is talking to a lender. Remember, the map says the area is eligible, but the property must also meet safety and habitability standards. The lender will order an appraisal to ensure the home is structurally sound. This is where the "final determination" disclaimer comes into play. The map gets you to the door; the lender and appraiser let you in. Keep records of your search. Screenshot the map result for your address. It shows your agent and lender that you’ve done your homework, speeding up the pre-approval process.

Common Pitfalls and Mistakes to Avoid

Even with the best intentions, buyers mess this up. One common error is assuming that all rural land qualifies. It doesn’t. The property must be a primary residence. You can’t use a USDA loan to buy a vacation home or a pure investment rental property that you won’t live in. You have to occupy the home. This is a strict rule. If you’re an investor looking to buy a second home to flip or rent out immediately without living there, this program isn’t for you. However, multi-unit properties (like duplexes) can qualify if you live in one unit.

Another pitfall is ignoring the income calculation nuances. People often forget to include certain types of income or misjudge the household size. If you have adult children living with you who contribute to household expenses, they might count toward the income limit. It’s complex. Always work with a lender who specializes in USDA loans. General mortgage brokers might not know the ins and outs of the 2026 guidelines. A specialist can help you structure your application to highlight your strengths and navigate any gray areas in your financial history.

Also, don’t wait until the last minute to check eligibility. In a hot market, homes sell fast. If you find a house you love, you need to know immediately if it qualifies. Waiting for the lender to check days later could cost you the deal. Make the map your first stop, not your last. And beware of outdated info. Articles from 2020 or 2021 might reference old boundaries or income limits. Stick to 2026-specific resources. The landscape changes, and relying on old data is a recipe for disappointment. Stay current, stay informed, and stay ahead of the curve.

So, what if you check the map and it’s a hard no? Or maybe your income is slightly over the limit? Don’t panic. There are other paths to homeownership. FHA loans are the most common alternative. They require a 3.5% down payment, which is still low compared to conventional loans, and they have more flexible credit requirements. While not zero-down, they’re accessible to many buyers who miss the USDA cut. Plus, FHA loans don’t have the same geographic restrictions, so you can buy anywhere.

Conventional loans are another option, especially if you have a strong credit score and some savings. With programs like 3% down conventional loans, you can get close to the USDA ease of entry. The trade-off is usually higher interest rates or private mortgage insurance (PMI), but for some, the freedom to buy in any location outweighs the cost. It’s about weighing your priorities. Do you value the zero-down feature more than location flexibility? Or vice versa?

There are also state and local first-time homebuyer programs. Many states offer down payment assistance grants or low-interest loans that can mimic the benefits of a USDA loan. These programs often have their own maps and eligibility criteria, sometimes targeting specific urban revitalization zones. It’s worth exploring these options with a local housing counselor. They can provide a holistic view of all the aid available to you. Just because USDA isn’t the right fit doesn’t mean homeownership is out of reach. It just means you need to pivot your strategy. Keep looking, keep asking questions, and don’t let one "no" stop your journey.

At the end of the day, the 2026 USDA Eligibility Map is more than just a digital tool. It’s a gateway. It represents a chance for thousands of Americans to achieve stability and build equity without the crushing burden of a massive upfront payment. Whether you’re drawn to the quiet charm of a true rural setting or the convenient buzz of an eligible suburb, the opportunity is there if you know where to look.

The key is to stay proactive. Use the map early and often. Verify your income status against the latest 2026 limits. Connect with lenders who understand the nuances of Rural Development loans. And remember, while the rules can seem rigid, the goal of the program is flexible: to help people find homes. Don’t let the complexity scare you off. Take it one step at a time. Check the address. Run the numbers. Ask the questions.

Homeownership is a marathon, not a sprint. The USDA loan is just one pair of shoes you can wear for the race. If they fit, great. Lace them up and go. If they don’t, there are plenty of other options waiting for you. But you’ll never know unless you check the map. So go ahead. Type in that address. See if it turns green. You might just find your future home waiting for you in the most unexpected place.